Efficient Markets

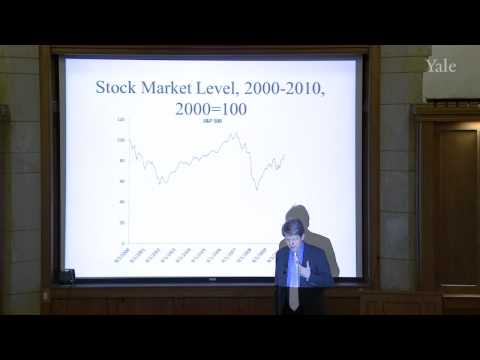

Robert Shiller, teaching Yale's Financial Markets course, examines whether markets truly price in all available information. He opens by revisiting David Swensen's guest lecture on the Sharpe ratio, noting how hard it is to measure standard deviation for illiquid assets and how some managers manipulate the ratio to flatter their returns. He then traces the history of the Efficient Markets Hypothesis, the idea that beating the market is impossible because prices already reflect public information, and tests it against technical analysis methods like the head and shoulders pattern. Shiller compares the Random Walk model of stock prices against a First-Order Autoregressive Process, arguing the latter fits real market behavior better. He closes by weighing this evidence alongside Swensen's own record of consistently outperforming the market, concluding that the Efficient Markets Hypothesis is, at best, a half-truth.