Portfolio Diversification and Supporting Financial Institutions

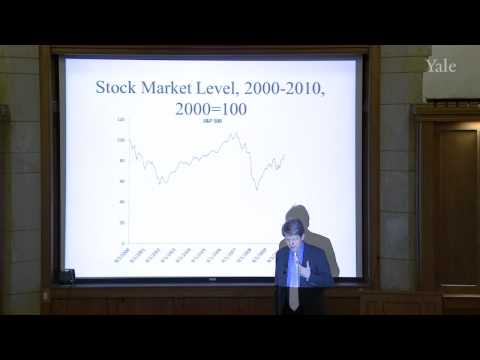

Robert Shiller, teaching Yale's Financial Markets course, lays out mean-variance portfolio analysis and the capital asset pricing model. He opens with the history of the United East India Company, founded in 1602 as the first publicly traded company, and traces the development of stock exchanges from Amsterdam onward. This leads into the equity premium puzzle, the unusually high historical returns of stock investments relative to bonds. Shiller then works through Harry Markowitz's original portfolio theory, showing how leverage trades off against risk and how an efficient portfolio frontier is constructed. He builds toward the tangency portfolio and the Mutual Fund Theorem, before closing with CAPM, which ties a stock's expected return to its exposure to market risk. The lecture combines historical narrative with the mathematical machinery of modern finance.