Risk and Financial Crises

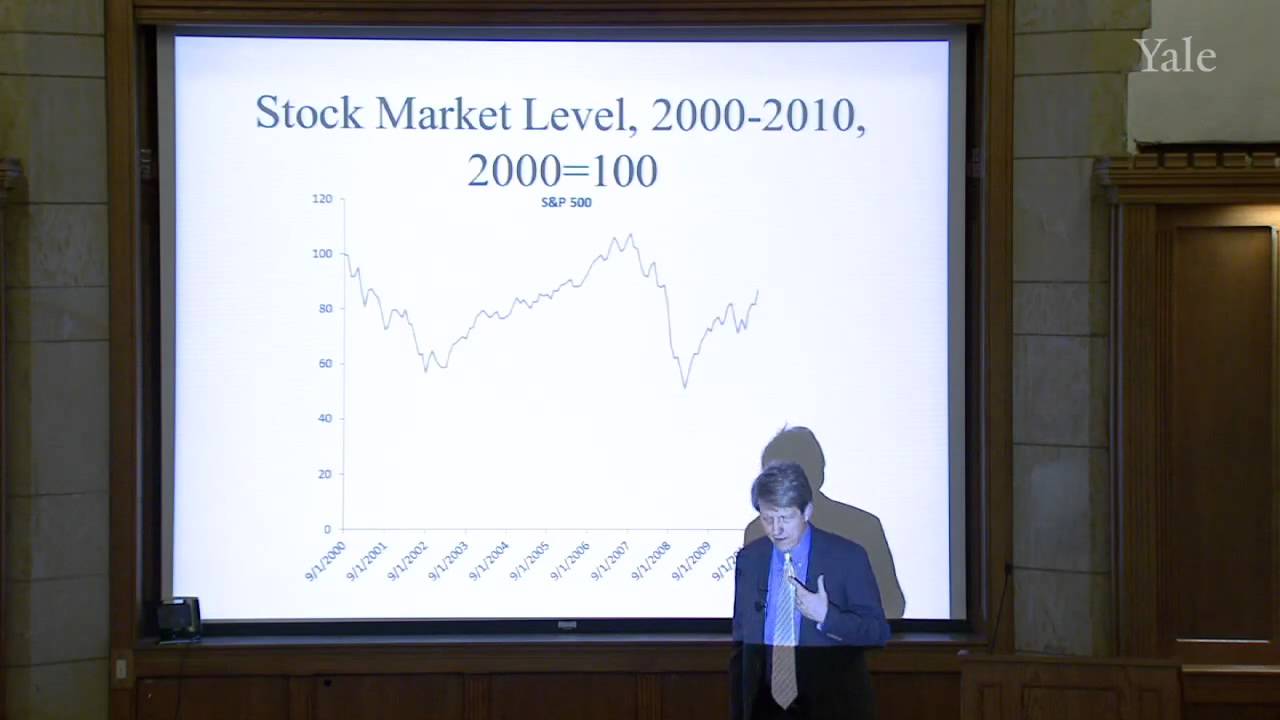

Robert Shiller opens Yale's Financial Markets course with the 2007-2008 crisis as a case study in probability theory. He walks through expected value, variance, covariance, and correlation of random variables, then shows how the law of large numbers depends on an independence assumption that broke down during the crisis, distorting Value at Risk calculations. He covers regression analysis on financial returns to split an asset's risk into systematic and idiosyncratic components, then closes by testing the normal distribution against actual stock market history. Outliers during crisis periods, he argues, occur far too often for returns to be normally distributed, pointing instead toward fat-tailed distributions. The lecture moves chapter by chapter from historical narrative into formal statistics, grounding each concept in market data rather than abstract examples.